Rate Cuts in Doubt, but Does It Matter?

April 17, 2024

Back in the fall of 2023, the Fed signaled that rate hikes were finished, prompting a significant stock market rally that has been largely uninterrupted. Thanks to softening inflation data, markets headed into 2024 quite certain that rate cuts were just around the corner, with the market consensus pointing to March 2024 for the first cut. A reversal of inflation data in January and February, showing higher prices, caused investors to push back the ETA on the first cut to June. This repricing barely registered as a blip in equity markets, however, as it aligned with the Fed’s own (more conservative) projections for three total 2024 cuts.

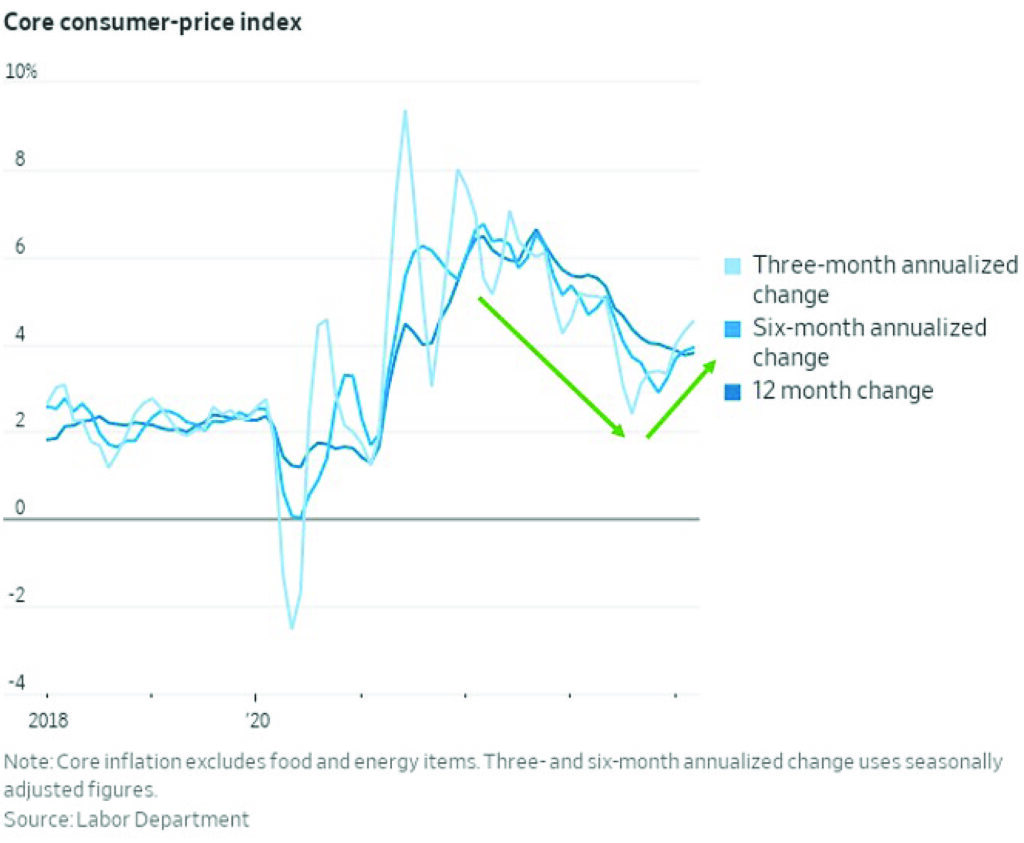

Prior to the March inflation data, the narrative was that the early 2024 inflation was merely a seasonal anomaly, and that inflation would likely resume softening. After March CPI data revealed a continuation in the trend of hotter-than-expected inflation, the timeline for inflation has become much more uncertain. Core CPI data now shows price increases accelerating in the three-, six-, and twelve-month time periods.

Exhibit 1. Core CPI Trends

While the March “Dot Plot” of Interest Rate Projections from the Fed still shows a consensus view of 3 rate cuts in 2024, the margin is razor-thin – a hawkish shift from just one or two Fed members could alter the consensus trajectory for rates. Minneapolis Fed President Neel Kashkari even raised the possibility of an additional rate hike this year. For their part, big banks aren’t waiting for the Fed to alter their forecast. Goldman Sachs, UBS, Wells Fargo, Nomura, and Evercore ISI all revised their outlook to just 50 basis points of cuts. Bank of America, Barclays, and Deutsche Bank went even further in now anticipating just a single 25 basis point cut.

The reaction from equity markets has been more tepid than some would expect. There has been a modest pullback from all-time highs and an uptick in 10-year Treasury yields back above 4.6%, but geopolitical tensions and election year uncertainty are also somewhat to blame. Lofty expectations for corporate earnings and consistently strong US economic data are providing reason for investors to stay in equity markets, although that same economic strength is also providing the Fed with rationale to delay rate cuts as long as possible.

Investors are in a precarious position – should they stay fully invested, awaiting the “pivot” moment when the Fed announces the first cut? Or is this the moment when the risk outweighs the reward, and should investors follow big banks’ lead and pre-empt a potential hawkish Fed rate revision? Comments from the Fed indicate that all things being equal, the central bank views the risk of entrenched inflation from cutting too early as a greater risk than an economic downturn from keeping rates pegged higher. Therefore, it is very possible that the June “Dot Plot” will end up showing two or fewer rate cuts as the consensus forecast.

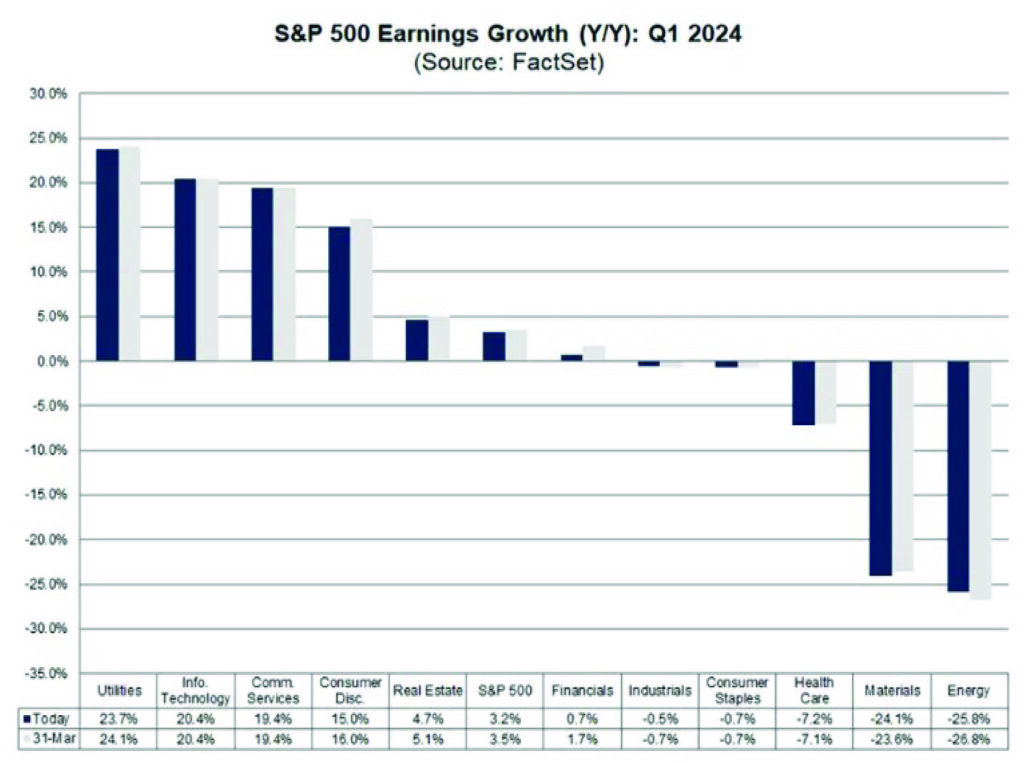

The good news for stock market bulls is that we will get two more months’ data of the Fed’s primary inflation gauge, Core PCE, before the Fed meets in June. We are also just beginning the first-quarter 2024 corporate earnings, which are expected to come in 3.2% higher than the previous year. As we have seen in previous quarters, strong corporate earnings have provided the impetus for investors to push stocks higher. With US large-cap companies currently holding record cash reserves, higher rates are unlikely to deter the mega-caps from engaging in capex spending or increasing dividends. Aside from the Utilities sector, it looks like Q1 will see a continuation of the “rich get richer” trend with growth-oriented sectors such as Tech and Communications Services once again outperforming.

Exhibit 2. EPS Growth Forecasts for the 11 US Equity Sectors as of 4/15/2024

Unfortunately, smaller cap stocks will likely have to wait, once again, for their moment as the “higher-for-longer” rate environment remains an impediment to investors reallocating to small and medium-sized firms, despite historically low relative valuations. Patient investors will still likely be rewarded with an eventual explosive move higher for small caps, but that timeline is hazy with the Fed outlook in flux.

There may be a tactical opportunity for investors to anticipate a hawkish Fed June revision and move some equity exposure to the sidelines, but we caution that any pullback could be brief and relatively shallow. Thus far, the resilience of the US economy has given the Fed a considerable lifeline to push off rate cuts. Presuming data on the economic front continues to surpass expectations and earnings once again deliver, we could be (hopefully) nearing a point where equity investors simply deem Fed policy irrelevant and dot plots become a footnote in financial news rather than the main event.

Thank you, as always, for the opportunity to serve you.

Read the Forbes article – Here

Vestbridge Advisors, Inc. (“VB”) Is registered with the US Securities and Exchange Commission as a registered investment advisor with principal offices at 3393 Bargaintown Road, Egg Harbor Township, NJ. The information contained in this publication is meant for informational purposes only and does not constitute a direct offer to any individual or entity for the sale of securities or advisory services. Advisory advice is provided to individuals and entities in those states in which VB is authorized to do business. For more detailed information on VB, please visit our website at www.Vestbridge.com and view our Privacy Policy and our ADV2 Disclosure Document that contains relevant information about VB. Although VB is a fairly new organization, any references herein to the experience of the firm and its staff relates to prior experience with affiliated and nonaffiliated entities in similar investment related activities. All statistical information contained herein was believed to be the most current available at the time of the publishing of this publication.