The Road to 2% Inflation

August 16, 2023

Up until the latest Consumer Price Index (CPI) inflation reading, the Fed had been on quite a winning streak. Annualized CPI had declined for 12 consecutive monthly readings, evidence that while prices for goods and services were still increasing, the pace of price inflation was moderating and moving back towards the Fed’s 2% target. Jerome Powell cautioned, however, that the path forward would not likely be a straight line and inflation could fluctuate as the effects of the Fed’s rate hikes work through the economy. The July CPI release showed a headline inflation uptick from 3.0% to 3.2%, which at first glance looks like we are suddenly going the wrong way. Has the Fed lost course? Or is this just an example of the fluctuation that Chairman Powell warned of?

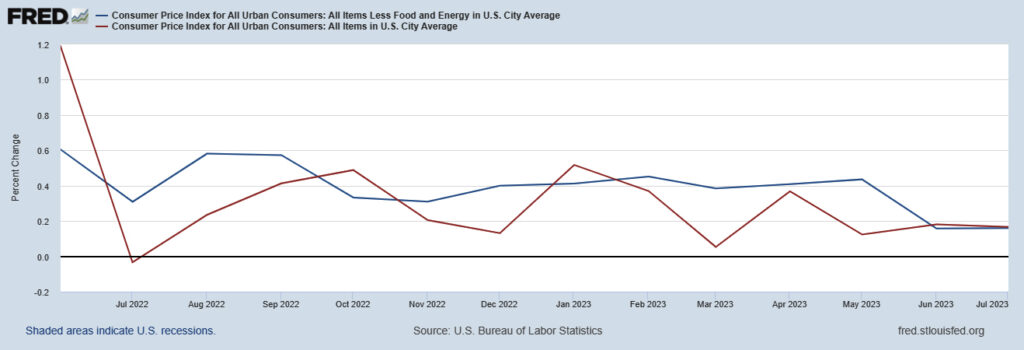

If we examine inflation monthly, we see evidence that inflation is more up-and-down than steady. The monthly data points are choppy, as shown in the below chart of CPI (Red Line) and Core CPI (Blue Line). Core CPI excludes Food and Energy prices due to their tendency to swing wildly on occasion due to outside influences such as natural disasters or geopolitical events.

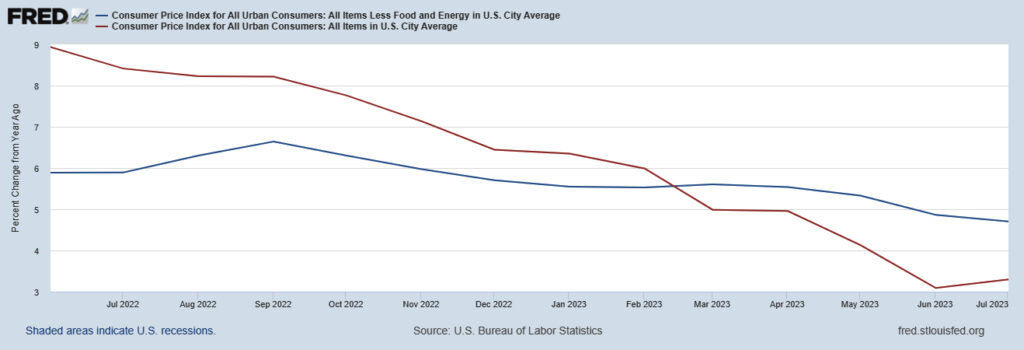

The annualized rate looks much smoother and shows the progress that the Fed and Biden administration have highlighted, with the red line showing headline CPI on the steady 12-month downtrend as previously mentioned. Core CPI also trended downwards, albeit at a flatter slope.

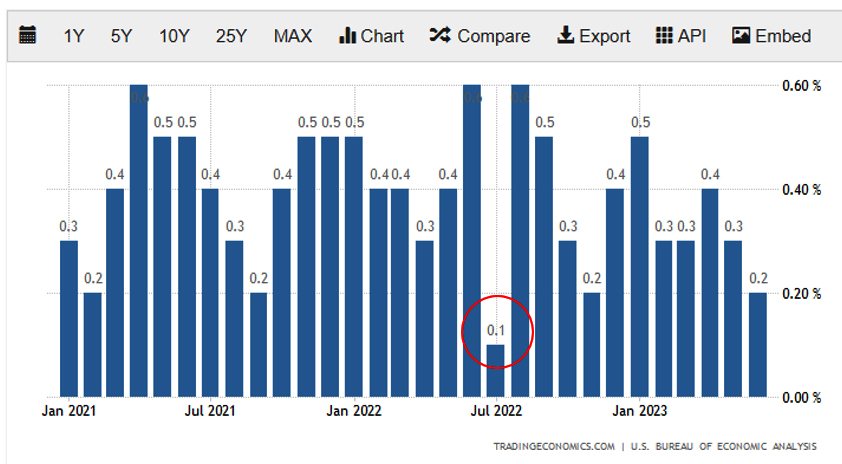

The slight upward reversal of headline CPI in July 2023 may seem concerning at first glance. However, if we look back at the monthly data, we can see a clear explanation. The July 2022 data point, in which CPI fell into deflationary territory, simply fell off the trailing 12-month annualized calculation. We refer to this as “base effect”, the phenomenon when a trailing data point which is abnormally low or high is removed from the trailing data and consequently creates a shift in the arithmetic calculation of the annualized data. July 2022 CPI was down sharply because Energy flipped from positive 6.9% in June 2022 to negative 4.7% in July 2022.

The Fed, of course, knows all of this, and likely is not concerned about their broken winning streak of decreasing CPI. While the Fed looks at CPI, their stated inflation measure is the Core Personal Consumption Expenditure Index (Core PCE). The next Core PCE release is August 31st, and we expect a similar hiccup in the annualized data, despite a projection from the Cleveland Fed of a quite encouraging 0.2% monthly reading.

This is because, like CPI, Core PCE had its best monthly reading at just 0.1% in July 2022, which will no longer be included in the July 2023 calculation.

Because of this base effect, the Cleveland Fed’s inflation forecasting model is currently expecting Core PCE to rise from an annualized 4.01% to 4.23%. The good news is barring an unexpected spike in monthly inflation data for August 2023 the 0.6% August 2022 data point will be the next one to fall out of the calculation, which will lower the annualized rate again.

The Fed has its hands full fighting inflation, as we previously mentioned (see our June commentary), there are larger inflationary demographic forces at play which rate hikes are either ill-suited to combat or may even exacerbate. Knowing the July setback can be attributed to the base effect and that the monthly data is still trending towards the 2% goal, we still expect the Fed to hold rates unchanged in September and possibly continue to pause in November and allow the base effect to work in its favor.

Thank you, as always, for the opportunity to serve you.

Read the Forbes article – Here

Vestbridge Advisors, Inc. (“VB”) Is registered with the US Securities and Exchange Commission as a registered investment advisor with principal offices at 3393 Bargaintown Road, Egg Harbor Township, NJ. The information contained in this publication is meant for informational purposes only and does not constitute a direct offer to any individual or entity for the sale of securities or advisory services. Advisory advice is provided to individuals and entities in those states in which VB is authorized to do business. For more detailed information on VB, please visit our website at www.Vestbridge.com and view our Privacy Policy and our ADV2 Disclosure Document that contains relevant information about VB. Although VB is a fairly new organization, any references herein to the experience of the firm and its staff relates to prior experience with affiliated and nonaffiliated entities in similar investment related activities. All statistical information contained herein was believed to be the most current available at the time of the publishing of this publication.