China’s “3D” Challenge: Deflation, Debt, and Demographics

August 24, 2023

The Federal Reserve Bank of Kansas City will hold its 46th annual Economic Policy Symposium this week in Jackson Hole, Wyoming. The theme, “Structural Shifts in the Global Economy”, will likely focus on the post-pandemic economic landscape, and how the significant lingering after-effects on global trade networks and government fiscal and monetary policies may alter the global economic system.

The US is the world’s largest economy, and China is 2nd. China has long been the driver of global economic growth, expanding at an average rate of over 9 percent per year since 1978. Recent economic data, however, indicates a significant slowdown for Chinese growth is occurring, reversing a brief period of outperformance as China rebounded from the Covid-19 lockdowns. 2023 Chinese GDP is now projected to be around 4.5% according to Barclays, not much higher than projected US GDP of 3%.

The Chinese government’s notoriously opaque and often incomplete economic data releases only increase uncertainty, as does the regime’s tendency to aggressively interfere in the affairs of publicly traded companies. The lack of transparency has led some in the financial industry to deem China “un-investable”, despite its significant global presence.

Due to the interconnected nature of global markets, and China’s role as the largest US trading partner, even investors who have avoided Chinese equity exposure need to be aware of the challenges facing the world’s most populous nation. We can broadly categorize some of the biggest issues facing China as Deflation, Debt, and Demographics.

Deflation: As global central banks desperately try to reign in runaway inflation, China is an anomaly with prices falling into deflationary territory in July. China’s July Consumer Price Index (CPI) fell to -0.3% year on year in July, while Producer Prices fell -4.4% annually. The deflationary data is the aftereffect of China’s response to the pandemic, which focused on reducing debt and reigning in speculative sectors of the market, in contrast to aggressive stimulus programs from the US and other developed nations. Some Chinese policy advisors are now calling for stimulus measures to boost consumption, lest China fall into a deflationary spiral as consumers delay purchases for goods and services. Just as inflation puts pressure on consumers to purchase goods today or else risk higher prices in the future, deflation discourages purchases since consumers expect goods to be cheaper in the future.

How does Chinese deflation affect the US? China may “export” its deflation by flooding the US market with relatively cheaper goods. On the surface this would be helpful in bringing down inflation in the US. Cheaper imports can create a decline in demand for domestic goods, which if left unchecked could result in reduced levels of manufacturing, business investment, and ultimately lower profits and higher unemployment. The Fed would welcome a moderate dose of economic cooling, but the situation at home could devolve into a recession if China can’t stem the price declines.

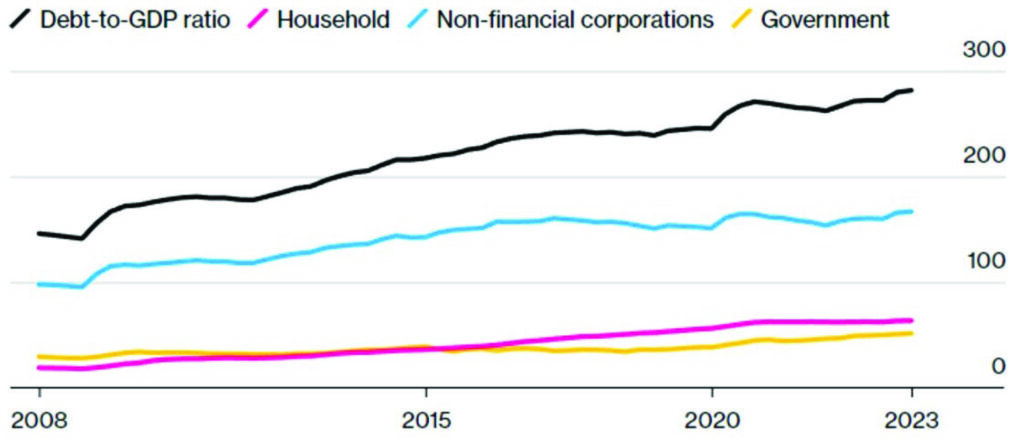

Debt: To understand the complexities of the Chinese relationship with debt, one must go back to the 2008 global financial crisis. To stimulate its economy, the Chinese government unleashed the equivalent of $587 billion in spending, which at the time equated to 12.5% of China’s GDP. On a relative basis, the stimulus was triple the measures implemented here in the US. That stimulus propelled a massive construction boom, as many questioned whether the empty “ghost cities” would ever be populated by the up-and-coming Chinese middle class. Today, the property sector accounts for 23% of Chinese GDP.

The Chinese government attempted to reign in the property bubble following the pandemic, stopping the flow of cheap money to real estate companies. Now the real estate sector is facing a string of defaults that only seems to be accelerating. Thus far, more than 50 Chinese developers have defaulted over the last three years. The sector’s struggles have exposed the scope of the Chinese “shadow banking” complex, which exists outside traditional banking regulations and systems. More than 40% of the country’s outstanding loans are tied to shadow banking activities, with the real estate developers such as the embattled Country Garden relying on financing from so-called Trust firms that are now also facing a liquidity crisis as property values decline.

The Chinese government may be reticent to bail out the property developers, as it has its own debt to deal with. The Chinese central bank has slashed interest rates to keep lending flowing, but thus far refrained from more direct stimulus measures. The government appears to be getting uncomfortable with the country’s total debt load, which has swelled to nearly 300% of GDP, eclipsing the debt-to-GDP ratios of the US and Eurozone. Economists estimate that to gain a dollar of GDP growth, China needs to invest $9 in government spending, highlighting the diminishing returns following decades of overdevelopment and infrastructure projects.

Exhibit 1. China Debt-to GDP, overall and components

Clearly, China can no longer rely on borrowing to build as the primary driver of GDP. Government officials are presently at odds over what the next evolution of the Chinese economy will look like. While some advocate for a Western-style economy to boost household spending on goods and services, the Xi regime is hesitant to embrace this idea, partially because it implies greater personal autonomy for citizens. Rather, the government is focusing on increasing Chinese market share in high-value, high-growth industries such as semiconductors and electric vehicles.

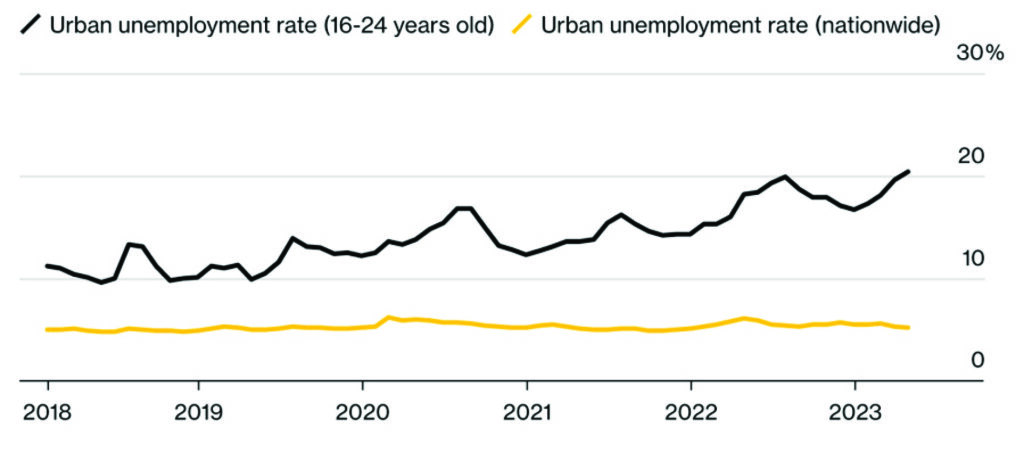

Demographics: China is challenged by an aging population, the result from decades of its “one-child” policy. UN projections forecast China will lose nearly 50% of its population by the end of this century. Among the youth, unemployment has soared, with the jobless rate for 16-to-24-year-olds hitting 21.3 percent in June, prompting the government to suspend reporting of the data in July. If the youth unemployment rate were expanded to account for non-students out of the workforce, some economists have estimated it may be closer to 50%.

Exhibit 2. Chinese Urban Unemployment and Youth Urban Unemployment Rates

The employment prospects for those over 35, who should be in the prime of their careers, are not much better. Chinese citizens refer to the “Curse of 35”, a common form of legal age-discrimination where employers avoid hiring workers over 35. Even civil service jobs typically bar workers over 35 from applying, making it difficult for many Chinese citizens to find steady, well-paying employment needed to start families and reverse the demographic trends.

For young, educated Chinese workers, there is a shortage of high-paying, high-skill jobs that Chinese college graduates are seeking. Chairman Xi Jinping has stated that these workers should seek employment in factories or in rural farmwork, but many are simply removing themselves from the workforce, a phenomenon known as “lying flat.” Others seek better employment prospects overseas, which only exacerbates the growing demographic imbalance.

What happens next? Despite its unwieldy debt burden, it seems likely that the Xi regime will need to implement some kind of economic stimulus to address deflation and joblessness to stem growing civil discontent. The form of that stimulus will take is uncertain. The biggest risk is if the regime chooses to refocus spending from infrastructure to its military pursuits, which could heighten global tensions. Taiwan is of crucial importance as a US trade partner and producer of 50% of the globe’s semiconductors. If Xi elects to increase aggression towards Taiwan it will have widespread global implications on supply chains and trigger a market selloff over the risk of military conflict.

The global economy is a complex, interconnected structure, and China remains a key component. Even for investors who choose to avoid exposure to Chinese equities, it is impossible to completely insulate portfolios from China due to supply chain dynamics. Maintaining awareness of the Chinese economy, and the changes and challenges it faces, is necessary to make informed asset allocation decisions and prepare for potential downside risks as the power dynamics shift in the global economy.

Direct investments in the overall China stock market remain questionable even for long term investors at this time.

Read the Forbes article – Here

Vestbridge Advisors, Inc. (“VB”) Is registered with the US Securities and Exchange Commission as a registered investment advisor with principal offices at 3393 Bargaintown Road, Egg Harbor Township, NJ. The information contained in this publication is meant for informational purposes only and does not constitute a direct offer to any individual or entity for the sale of securities or advisory services. Advisory advice is provided to individuals and entities in those states in which VB is authorized to do business. For more detailed information on VB, please visit our website at www.Vestbridge.com and view our Privacy Policy and our ADV2 Disclosure Document that contains relevant information about VB. Although VB is a fairly new organization, any references herein to the experience of the firm and its staff relates to prior experience with affiliated and nonaffiliated entities in similar investment related activities. All statistical information contained herein was believed to be the most current available at the time of the publishing of this publication.