State of the Consumer

May 25, 2023

In our Annual Outlook for 2023, we raised the possibility that the US economy could potentially avert recession in 2023, powered by full employment and robust consumer spending. Thus far, with roughly a month left in the 2nd quarter, the US economy has proven itself surprisingly resilient, with GDP growth of 1.3% in Q1 and unemployment at just 3.4% in April. The economic growth in the first quarter was largely attributable to strong consumer spending despite persistent price increases for both goods and services. The US consumer’s willingness to absorb price increases passed on by corporations has created an environment of record-high profit margins and resulted in strong first quarter 2023 earnings with over 76% of S&P 500 companies beating analysts’ expectations, the best rate since Q1 of 2022.

If the fate of the US economy rests in the hands of the American consumer, there could be major trouble on the horizon, as warning signs are starting to appear in several indicators. There is growing evidence that the US consumer is close to tapped out, and if so, we could finally see an earnings recession in the latter half of the year, which could spiral into an economic recession while the Fed still struggles to make headway on inflation. In this commentary, we will examine why consumers have been so willing to spend, and what could trigger them to cut back in the coming months.

Economists initially attributed the uptick in consumer spending to pandemic stimulus measures. During the pandemic, many US taxpayers were eligible for direct Economic Impact Payments of $1,200 for individuals and $2,400 for married couples, plus $500 per dependent. More than 160 million such payments were made, totaling $269 billion. Expanded unemployment payments were also made, totaling around $260 billion. Other programs, such as moratoriums on foreclosures and evictions and the Paycheck Protection Program (PPP), provided lifelines to renters, homeowners, and small business owners during the depths of the pandemic.

Those stimulus programs have since ceased, and the monetary payments have likely worked their way through the economy. Consumers who cut back spending during the pandemic made up for lost time with a demand surge for goods, dining experiences, and vacations. This rapid uptick in spending is the driving force behind both the low unemployment and high inflation numbers. Consumer demand prompts employers to hire more workers and raise pay, which results in discretionary spending from those workers, in an inflationary feedback loop that has confounded the Fed.

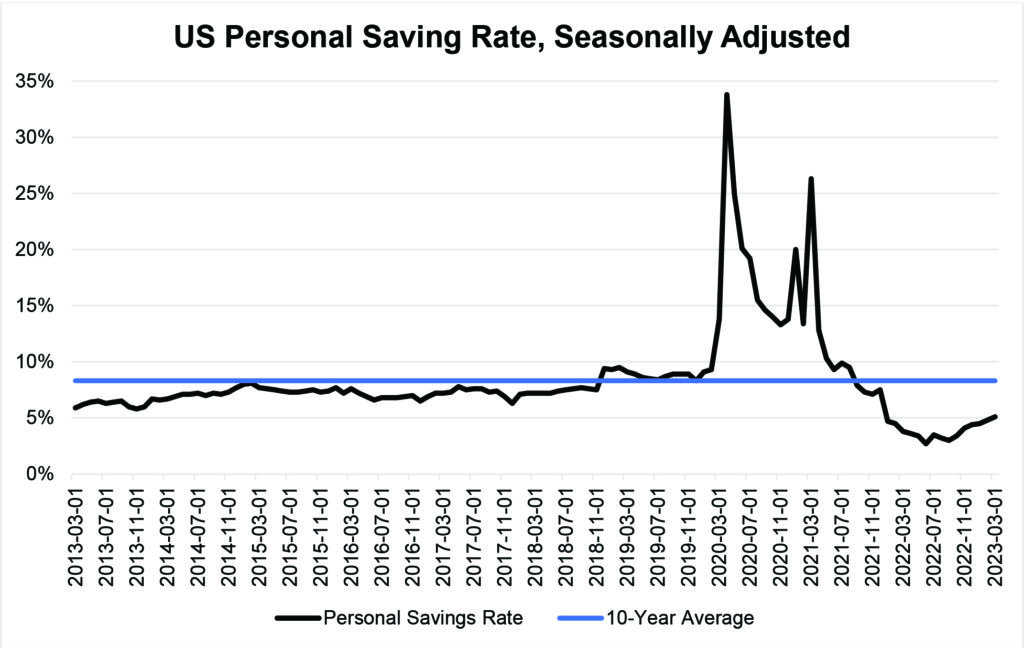

That said, the surplus savings accumulated during 2020-2021 have evaporated, pushing the personal savings rate down below pre-pandemic levels.

Exhibit 1: US Personal Savings Rate

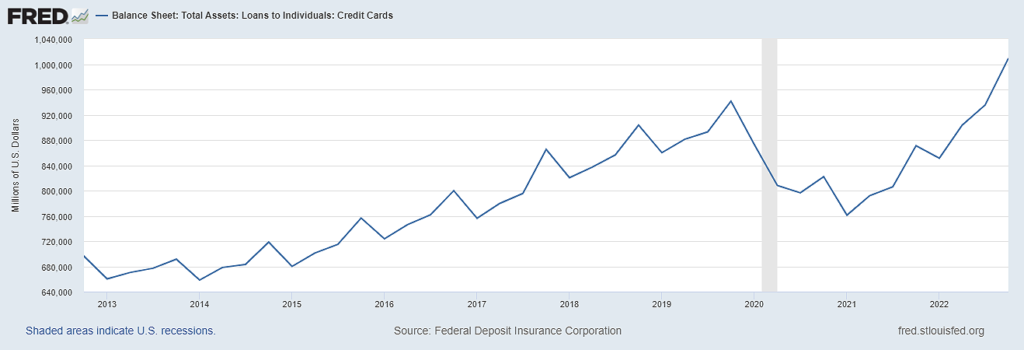

If consumers are out of savings, but still spending, it means they are taking on more credit card debt, and data shows credit card balances have eclipsed $1 Trillion to reach a new all-time high. For more than a third of US adults, outstanding credit card debt now exceeds their personal savings according to a recent report by Bankrate.com. Furthermore, the cost of carrying those credit card balances has risen, with the average credit card interest rate over 20% for all existing accounts and over 22% for new accounts according to WalletHub.com.

Exhibit 2: Outstanding Credit Card Balances

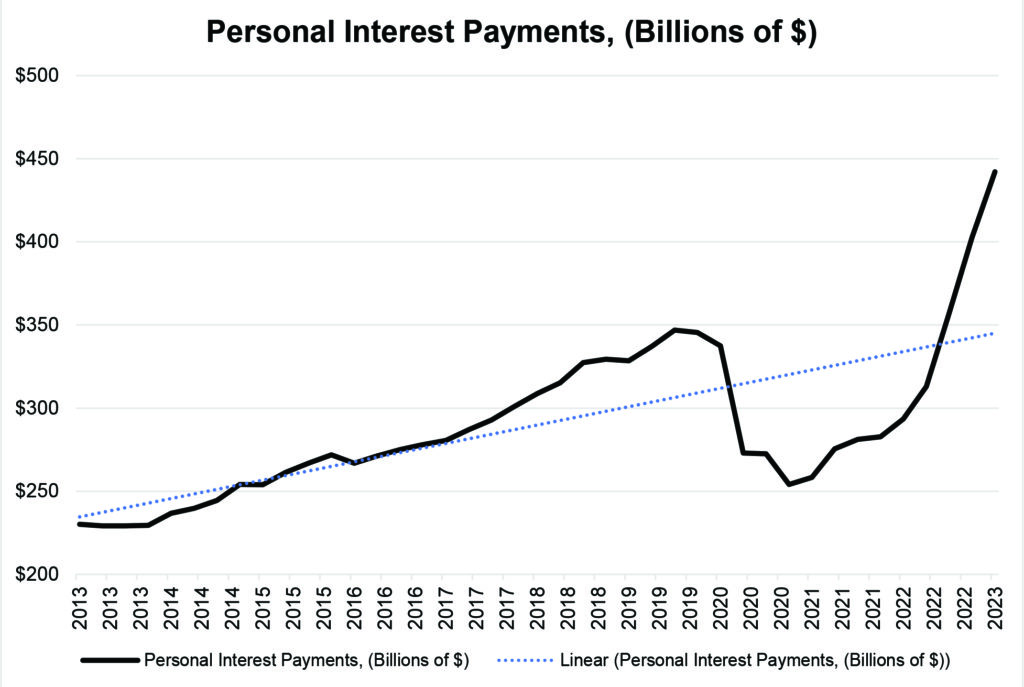

Data from the US Bureau of Economic Analysis shows that consumers appear to be taking on an unsustainable amount of personal debt. Personal Interest payments from US Consumers had fallen below the trendline (blue dotted line on below chart) following COVID thanks to decreased spending and ultra-low interest rates. But since 2022, interest payments have increased dramatically, as evidenced by the sharp upward slope nearing $450 billion annually.

Exhibit 3: US Personal Interest Payments

Additionally, there is another shoe yet to drop while US consumers are saving less, spending more, and incurring significantly higher interest charges for their debt burdens. 43.5 million US citizens are about to get another monthly bill as the student loan moratorium nears its expiration and loan forgiveness measures face an uncertain fate.

During the pandemic, the US government implemented a pause on student loan principal and interest payments for most federal student loan borrowers, which was originally set to expire on September 30, 2021 but has been extended multiple times. Meanwhile, President Biden campaigned on a separate measure to forgive up to $20,000 for qualifying borrowers, a key promise that helped him shore up the youth vote and win the presidency. Republican lawmakers have sought to stop the $20,000 forgiveness program, although Biden has vowed to veto any resolution from Congress. Ultimately, the fate of the forgiveness program is in the hands of the Supreme Court, which is expected to make its ruling in late June or early July.

Regardless of the outcome of the forgiveness program, student loan payments and interest accruals will resume within 60 days of the resolution of the litigation. If the litigation is not resolved by June 30th, payments will resume 60 days after, on August 29, 2023.

The paused student loan payments have been an ongoing stimulus measure for the 43.5 million borrowers with federal loans. After roughly 3 years of forbearance, many of these borrowers have likely grown accustomed to the extra money in their budgets and will need to cut back from either discretionary spending or reduce their personal savings when payments resume. The average federal student loan payment is $267 for a bachelor’s degree and $567 for a master’s degree, at an average interest rate of 5.8%.

While the $20,000 loan forgiveness would help reduce the student loan tsunami, the average federal student loan balance is $37,574, and the plan does nothing to help borrowers currently accumulating debt or resolve the larger issue of college tuition costs outpacing inflation by about 5x since 1970. The Department of Education is seeking to address some of these issues with an income-driven repayment proposal, which would cap or forgive student loan debt in some instances, but this is only in the proposal stage and given the resistance to other student loan forgiveness proposals, will face significant opposition.

Many of the 43.5 million borrowers likely have not adequately budgeted for the resumption of student loans after the lengthy three-year moratorium. Many also have likely taken on additional debt for vehicles or homes during this period and will face difficult decisions as they account for a new, significant monthly expense. It is very possible that shortly after the student loan repayments resume, we see an uptick in vehicle repossessions and possibly mortgage defaults

After first quarter earnings proved resilient, many investors are hoping that the widely projected decline in corporate earnings had been averted. Stocks, especially growth-oriented ones, have rallied nicely year-to-date in hopes that high margins and growing earnings are here to stay. But if consumers are maxing out their credit cards and overextending household budgets, eventually the spending will stop. If the US consumer taps out, an earnings downturn could show up when companies report after mid-year. In that scenario, it would be up to the Fed to rescue the stock market once again with rate cuts, although investors may be underestimating the central bank’s resolve to keep rates higher for longer given the stickiness of inflation data.

It is hard to imagine a recession with 3.4% unemployment, but things can change quickly when economic growth is being financed on a 22% interest rate credit card. Investors should keep a close eye on credit card and mortgage delinquencies, automobile repossessions, and other leading indicators because the debt will come due eventually, and US consumers may be nearly maxed out.

Thank you, as always, for the opportunity to serve you.

Vestbridge Advisors, Inc. (“VB”) Is registered with the US Securities and Exchange Commission as a registered investment advisor with principal offices at 3393 Bargaintown Road, Egg Harbor Township, NJ. The information contained in this publication is meant for informational purposes only and does not constitute a direct offer to any individual or entity for the sale of securities or advisory services. Advisory advice is provided to individuals and entities in those states in which VB is authorized to do business. For more detailed information on VB, please visit our website at www.Vestbridge.com and view our Privacy Policy and our ADV2 Disclosure Document that contains relevant information about VB. Although VB is a fairly new organization, any references herein to the experience of the firm and its staff relates to prior experience with affiliated and nonaffiliated entities in similar investment related activities. All statistical information contained herein was believed to be the most current available at the time of the publishing of this publication.