10-Year Break-out or Fake-out?

October 26, 2023

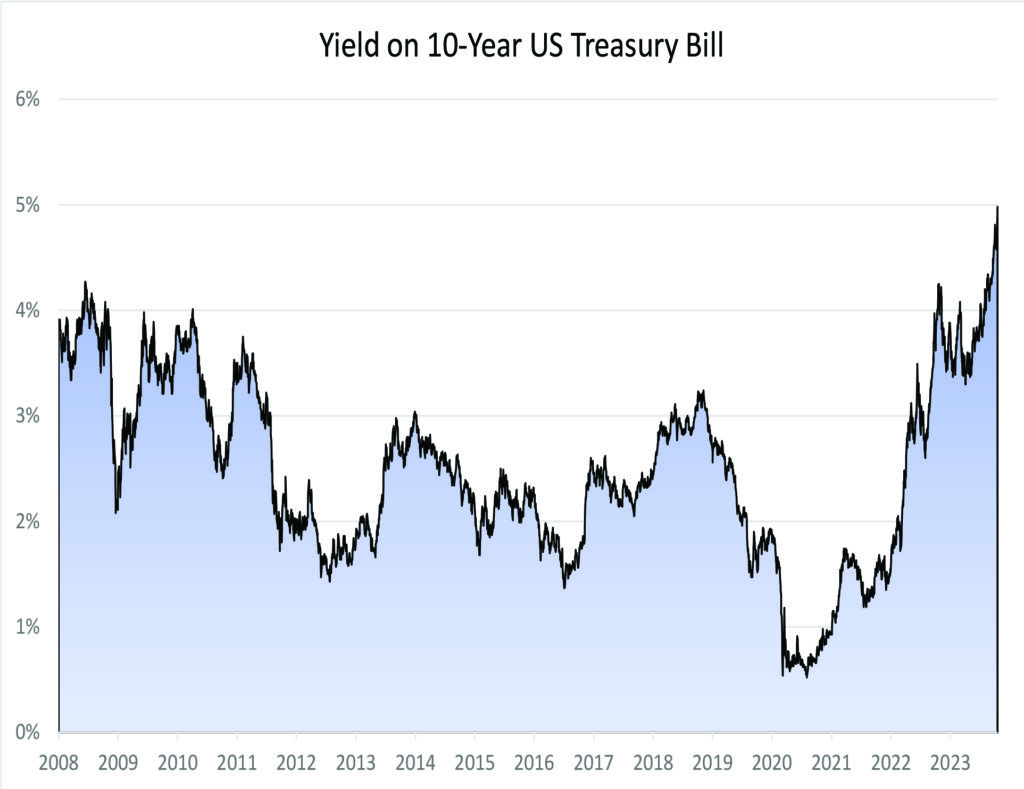

It’s rare for the bond market to dominate headlines versus stocks, but that is the case lately as the 10-Year US Treasury yield has tested 5%. While short term US Treasury yields have been well above 5% for months, the long end of the yield curve has been lower than the short end, causing what is known as an inverted yield curve. An inverted yield curve is typically the precursor to a recession since investors are anticipating deteriorating economic conditions sometime in the not-too-distant future that would trigger a flight to safety and lower long-term rates.

This was the narrative a year ago, when Bloomberg Economics proclaimed their model projected a 100% chance of recession within one year. Major Wall Street banks also called for a near-certain recession, with JP Morgan’s Jamie Dimon infamously warning investors to brace for an “economic hurricane.” Jamie likes to “talk his book”, a Wall Street term meaning whatever Jamie says typically is good for the business of, and stock price of, JP Morgan. Since these grim forecasts, however, the US economy has continued to churn out consistently strong data and persistent low unemployment. This is the optimistic explanation for the rise in the 10-year; capitulation of the doom-and-gloom crowd where they finally accept diminished recession risk. If investors don’t foresee recession on the horizon, equities look more attractive on a relative basis, reducing the demand for long-term risk-free government bonds and driving up rates.

Exhibit 1. Yield on 10-Year Treasury Bill

This rosy view is only one explanation. The actual cause of the 10-Year’s upward move is likely attributable to a combination of factors, not all positive.

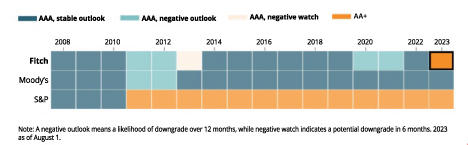

A more concerning catalyst for higher long-term rates, which was the subject of our recent commentary, is the unsustainable level of US government spending. The repeated debt ceiling showdowns and recent turmoil in the House of Representatives stem from the inability of both major political parties to reign in US government spending. The government dysfunction has led to a negative feedback loop of sorts, with excessive spending and congressional theatrics prompting downgrades of the US sovereign debt rating, and a lower sovereign debt rating then leading buyers to demand a higher rate as compensation. With the Fed already raising rates, the diminished creditworthiness of the US worsens an already bad situation, driving the cost of the interest on the nation’s debt higher. Congress has consistently opted to kick the can down the road rather than balance the budget and bond buyers are taking note and reassessing the cost of holding “risk-free” US bonds.

Exhibit 2. Historical US Sovereign Credit Rating – Fitch, Moody’s, and S&P

As the “risk-free” nature of US bonds has been called into question, there is also a lack of buyers in the marketplace due to two reasons. The first is the end of the Federal Reserve’s Quantitative Easing (QE) program. From June 2020 to October 2021, the Fed was buying $80 billion in Treasury securities and $40 billion of agency mortgage-backed securities (MBS) every month. The Fed tapered and ultimately ceased buying bonds in March of 2022. Thus far, there hasn’t been a major liquidity event because foreign governments have picked up the slack.

Foreign governments may be reassessing how much US debt they wish to hold on their balance sheets, however. In August, China unloaded over $21 billion in US bonds, the most in four years, bringing total holdings to $805 billion, the lowest amount since May 2009. Japan remains the largest foreign sovereign holder of US Treasuries, but with both China and Japan seeking to shore up their respective currencies against the dollar, that trend could shift, further diminishing liquidity.

Figure 3. Chinese Holdings of US Long-Term Treasuries

Bond markets are sophisticated and complex with many stakeholders, each with differing goals and priorities. A reversion of the yield curve from inverted to a normal, upward sloping one can be viewed as a positive event because it means recession is less likely. But higher long-term rates also bring challenges for a federal government which has been amassing a concerning level of debt. At the end of October, the Treasury Department will announce the Quarterly Refunding, the amount of Treasuries auctioned off to replenish its cash holdings and service the growing budget deficit. The announcement happens to coincide with the Federal Reserve Open Market Committee meeting and could be a catalyst for the next move up in rates. It seems likely that bonds will remain in the spotlight for a while longer.

Read the Forbes article – Here

Vestbridge Advisors, Inc. (“VB”) Is registered with the US Securities and Exchange Commission as a registered investment advisor with principal offices at 3393 Bargaintown Road, Egg Harbor Township, NJ. The information contained in this publication is meant for informational purposes only and does not constitute a direct offer to any individual or entity for the sale of securities or advisory services. Advisory advice is provided to individuals and entities in those states in which VB is authorized to do business. For more detailed information on VB, please visit our website at www.Vestbridge.com and view our Privacy Policy and our ADV2 Disclosure Document that contains relevant information about VB. Although VB is a fairly new organization, any references herein to the experience of the firm and its staff relates to prior experience with affiliated and nonaffiliated entities in similar investment related activities. All statistical information contained herein was believed to be the most current available at the time of the publishing of this publication.