Earnings Down, Stocks Up?

January 26, 2023

We are in the midst of fourth quarter 2022 earnings reporting season, with big banks having already reported and big tech results imminent. The consensus opinion of the market is that we are in for some underwhelming results, in both Q4 of 2022 and for at least the first quarter of 2023. This has been the theme for much of the year-long bear market – earnings expectations are too high and need to be adjusted.

Standard and Poors projects 2022 Earnings Per Share (EPS) to finish at just under $200 on the S&P 500, giving the index a PE around 19x. This would be a roughly 4% decrease from 2021’s $208.20 EPS. For 2023, Standard and Poors projects EPS of $224.57, which equates to 13% earnings growth during a year in which a recession is anticipated. Some investors see this as evidence that earnings estimates for 2023 are too optimistic and therefore due for a downward revision. What they may not realize is that these 2023 estimates have already been slashed nearly 10% since June, when Standard and Poors forecast EPS of $248. We could see another 10% downward revision to a flat 2023, but surprisingly, this may not trigger the major selloff in stocks that one would expect.

This is because markets are always looking forward to the next several quarters, which is why guidance often trumps trailing earnings results. This was illustrated by Microsoft (MSFT) earnings this week, in which the tech giant beat estimates and posted solid 31% growth in its Azure cloud business segment. Shares initially popped but then sold off after leadership gave a downbeat outlook for the coming year. Investors were more interested in where growth was headed than what it was in the past quarter.

This forward-looking mentality also applies to recoveries, however, and with the anticipated recession projected to be relatively benign, the bulk of the downward earnings adjustments may already be priced in. Therefore, do not be surprised if reactionary earnings-driven selloffs are met with swift buying pressure, as investors finally put their substantial cash reserves to work in anticipation of the 2nd half recovery expected in 2023. Stagnant or negative earnings growth does not necessarily equate to negative equity market returns.

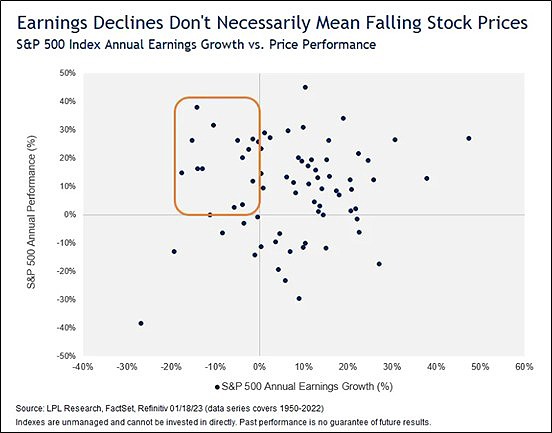

The below chart from LPL Research illustrates this phenomenon, with the S&P 500 posting positive returns more often than negative ones in years where EPS growth declines.

While there are numerous years in which EPS growth and stock market performance are both negative, the stock market more frequently shrugs off these EPS declines. With many stocks still down significantly from their prior highs, much of the selling may be behind us, and therefore bad earnings news may be an opportunity to establish positions in quality companies in anticipation of the market recovery.